HSAs in 2026: Maximize Your $4,150 for Triple Tax Benefits

Latest developments on Health Savings Accounts (HSAs) in 2026: Maximizing Your $4,150 Contribution for Triple Tax Benefits, with key facts, verified sources and what readers need to monitor next in Estados Unidos, presented clearly in Inglês (Estados Unidos) (en-US).

Health Savings Accounts (HSAs) in 2026: Maximizing Your $4,150 Contribution for Triple Tax Benefits is shaping today’s agenda with new details released by officials and industry sources. This update prioritizes what changed, why it matters and what to watch next, in a straightforward news format.

The current financial landscape and evolving healthcare costs make understanding and leveraging Health Savings Accounts more critical than ever. As we approach 2026, new contribution limits and strategic considerations come into focus. This article provides a comprehensive overview of how individuals can optimize their HSA for unparalleled financial advantages.

Understanding the 2026 HSA Landscape: New Contribution Limits

The Internal Revenue Service (IRS) has announced crucial adjustments for Health Savings Accounts (HSAs) in 2026, impacting how individuals can save for healthcare expenses. These changes include an increase in the maximum allowable contribution, presenting new opportunities for eligible participants.

For individuals, the annual contribution limit for Health Savings Accounts (HSAs) is set to rise, with a significant figure of $4,150 for self-only coverage. This adjustment reflects ongoing inflation and the rising costs associated with medical care, allowing account holders to set aside more pre-tax dollars.

Family coverage limits are also expected to see a proportional increase, making HSAs an even more powerful tool for households managing healthcare expenditures. These updated limits are essential for anyone planning their financial strategy for the coming years.

Eligibility Requirements for Health Savings Accounts (HSAs)

To qualify for a Health Savings Account (HSA), individuals must be enrolled in a High-Deductible Health Plan (HDHP) and not be covered by any other non-HDHP health insurance. This foundational requirement ensures that HSAs are utilized by those facing higher out-of-pocket costs before their insurance coverage fully kicks in.

Furthermore, an individual cannot be enrolled in Medicare, nor can they be claimed as a dependent on someone else’s tax return. Adhering to these strict eligibility criteria is paramount for opening and maintaining a compliant Health Savings Account (HSA).

It is vital for prospective HSA holders to review their current health insurance policies and personal circumstances carefully to confirm eligibility. Consulting with a financial advisor or an insurance professional can clarify any uncertainties regarding these requirements.

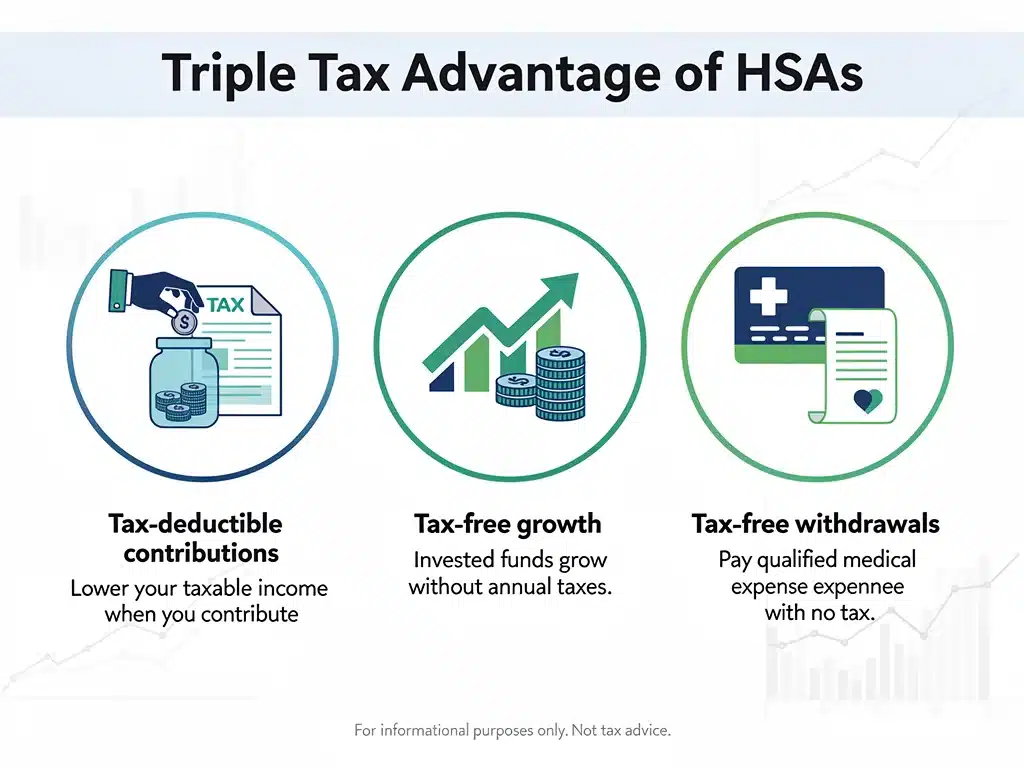

The Triple Tax Advantage: Unpacking HSA Benefits

Health Savings Accounts (HSAs) offer a unique and powerful “triple tax advantage” that sets them apart from other savings vehicles. This benefit structure is a primary reason for their growing popularity among financially savvy individuals.

Firstly, contributions to an HSA are tax-deductible, meaning they reduce your taxable income in the year they are made. This immediate tax break provides a direct financial incentive to fund your Health Savings Account (HSA) generously.

Secondly, the funds within an HSA grow tax-free through investments, similar to a 401(k) or IRA. This allows your savings to compound over time without being eroded by annual taxes on gains, a significant long-term benefit. Thirdly, qualified withdrawals for medical expenses are entirely tax-free, completing the triple advantage. This means you pay no taxes on the money when it goes in, while it grows, or when it comes out for eligible healthcare costs.

Maximizing Your $4,150 Contribution: Strategic Approaches

With the 2026 individual contribution limit at $4,150, strategic planning becomes crucial for maximizing the benefits of your Health Savings Account (HSA). This involves not just contributing the maximum, but also considering how and when to use the funds.

One effective strategy is to pay for current medical expenses out-of-pocket and allow your HSA funds to grow untouched for as long as possible. This approach leverages the tax-free growth component, turning your Health Savings Account (HSA) into a long-term investment vehicle.

Consider investing your HSA funds in a diversified portfolio, as many HSA providers offer investment options beyond basic savings accounts. Over decades, this investment growth can significantly enhance your financial security, especially for retirement healthcare costs.

Long-Term Investment Strategies

- Identify providers offering robust investment platforms for your Health Savings Account (HSA).

- Diversify your investments across various asset classes to mitigate risk and maximize potential returns.

- Regularly review and rebalance your HSA investment portfolio to align with your long-term financial goals and risk tolerance.

Another powerful strategy is to save all your medical expense receipts, even if you pay for them with other funds. You can then reimburse yourself tax-free from your Health Savings Account (HSA) at any point in the future, even years later, allowing your investments to grow longer.

This method effectively turns your HSA into an emergency fund for medical costs that can be tapped into when needed, while still enjoying the investment growth. It provides incredible flexibility and liquidity for both immediate and future healthcare needs.

HSAs as a Retirement Savings Vehicle

Beyond immediate healthcare needs, Health Savings Accounts (HSAs) are increasingly recognized as powerful retirement savings tools. Their unique tax structure makes them an excellent complement to traditional retirement accounts like 401(k)s and IRAs.

Once you reach age 65, your HSA funds can be withdrawn for any purpose without penalty, though non-medical withdrawals will be taxed as ordinary income. This flexibility essentially transforms your Health Savings Account (HSA) into another retirement account, offering a safety net for healthcare costs or other needs.

The ability to pay for qualified medical expenses tax-free in retirement is particularly valuable, as healthcare costs typically increase significantly in later life. This aspect alone makes the Health Savings Account (HSA) a cornerstone of comprehensive retirement planning.

Integrating HSAs with Retirement Planning

- Prioritize maximizing contributions to your Health Savings Account (HSA) annually, alongside your 401(k) or IRA.

- Utilize the HSA to cover rising Medicare premiums and other out-of-pocket medical costs in retirement.

- Consider the HSA as a flexible component of your post-65 income strategy, offering tax-free withdrawals for healthcare or taxable income for other expenses.

Many financial experts now advocate for maximizing HSA contributions before even fully funding a 401(k) or IRA, due to the superior tax advantages. This approach ensures that a significant portion of future healthcare costs can be covered with pre-tax, tax-free growth, and tax-free withdrawal funds.

The strategic use of Health Savings Accounts (HSAs) for retirement planning can lead to substantial savings and peace of mind. It’s a compelling option for those looking to build a robust financial future, free from the burden of escalating medical expenses.

Common Misconceptions and Clarifications

Despite their clear benefits, several misconceptions surround Health Savings Accounts (HSAs) that can deter potential users. Clarifying these points is essential for individuals to fully understand and utilize this valuable financial tool effectively.

One common misunderstanding is that HSA funds must be spent each year or they will be lost. In reality, HSA funds roll over year after year, accumulating indefinitely, making them a true long-term savings vehicle, unlike Flexible Spending Accounts (FSAs).

Another misconception is that HSAs are only for those who are healthy and rarely need medical care. While healthy individuals can benefit greatly from the investment growth, HSAs are also invaluable for those with chronic conditions, providing a tax-advantaged way to pay for ongoing medical expenses.

The Future Outlook for Health Savings Accounts (HSAs)

The trajectory for Health Savings Accounts (HSAs) appears robust, with continued policy support and increasing recognition of their value in a complex healthcare system. Experts anticipate ongoing adjustments to contribution limits to keep pace with inflation and healthcare costs.

As healthcare expenses continue to rise, the role of HSAs as a primary tool for managing these costs will only become more pronounced. This trend suggests that Health Savings Accounts (HSAs) will remain a cornerstone of personal finance for many years to come.

Legislative discussions may also focus on expanding eligibility or enhancing the features of HSAs, further solidifying their position. Staying informed of these potential changes is key for optimizing your Health Savings Account (HSA) strategy.

Navigating Provider Options and Fees

Choosing the right Health Savings Account (HSA) provider is a critical decision that can significantly impact your account’s growth and accessibility. Providers vary widely in terms of fees, investment options, and customer service quality.

It is important to compare administrative fees, investment management fees, and any other charges that might erode your savings. A low-fee provider can make a substantial difference in the long-term performance of your Health Savings Account (HSA).

Evaluate the investment platforms offered, looking for a diverse range of funds and user-friendly interfaces. The ability to easily manage and grow your Health Savings Account (HSA) funds effectively is paramount for maximizing its potential.

| Key Point | Brief Description |

|---|---|

| 2026 Contribution Limit | Individual limit set at $4,150, offering increased savings potential. |

| Triple Tax Advantage | Tax-deductible contributions, tax-free growth, and tax-free withdrawals. |

| Retirement Tool | HSA funds can be used for non-medical expenses post-65, taxed as income. |

| Strategic Investing | Pay out-of-pocket for medical costs to allow HSA funds to grow tax-free. |

Frequently Asked Questions About Health Savings Accounts (HSAs) in 2026

For 2026, the maximum individual contribution to a Health Savings Account (HSA) is projected to be $4,150. This amount is subject to final IRS confirmation but reflects expected adjustments for inflation and healthcare costs. It’s a key figure for planning your contributions.

Health Savings Accounts (HSAs) offer a triple tax advantage: contributions are tax-deductible, funds grow tax-free, and withdrawals for qualified medical expenses are tax-free. This combination makes HSAs an incredibly efficient savings and investment vehicle.

Yes, many Health Savings Account (HSA) providers offer investment options, allowing your funds to grow tax-free. Investing your HSA can significantly increase its value over time, especially if you pay for current medical expenses out-of-pocket and let the account compound.

Unlike Flexible Spending Accounts (FSAs), Health Savings Account (HSA) funds roll over year after year and never expire. This means you can accumulate substantial savings over time, making it a powerful tool for future healthcare expenses, including those in retirement.

After age 65, Health Savings Account (HSA) funds can be withdrawn for any purpose without penalty, functioning much like a traditional IRA. Withdrawals for non-medical expenses are taxed as ordinary income, while qualified medical expenses remain tax-free.

Looking Ahead: Strategic Financial Health with HSAs

The adjustments to Health Savings Accounts (HSAs) in 2026, particularly the $4,150 individual contribution limit, underscore their evolving role in personal finance. As healthcare costs continue to be a significant concern, the triple tax advantage offered by HSAs positions them as an indispensable tool for both immediate and long-term financial planning. Individuals should proactively assess their eligibility, maximize contributions, and strategically invest to leverage these benefits fully. The focus remains on informed decision-making to harness the full potential of your Health Savings Account in 2026, ensuring robust financial health for years to come.

in 2026: Boost Retirement Savings")